If the Beta for Stock a Equals Zero Then

A beta of 05 or -05 implies volatility one-half the benchmark. If the Beta for Stock X equals zero then according to the CAPM.

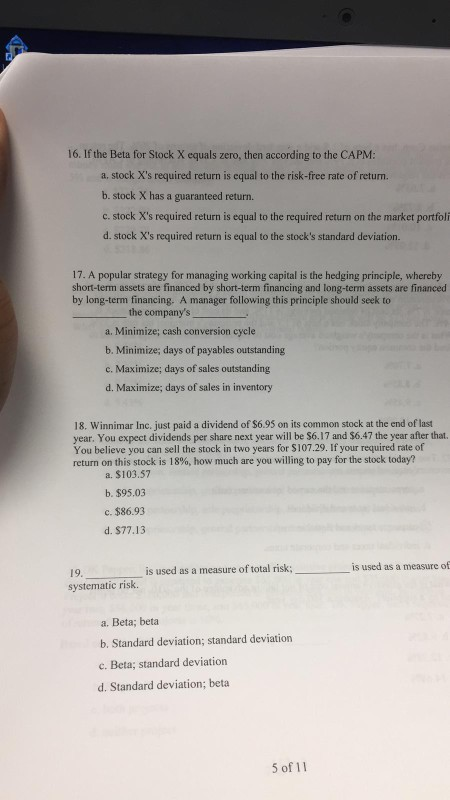

Solved 16 If The Beta For Stock X Equals Zero Then Chegg Com

C stock A has a guaranteed return.

. Note that if you only rebalance when portfolio beta goes outside of -03 03 rather than -015 015 you only need 618 trades 48. Stock As required return is greater than the required return on the market portfolio. Input the above numbers in the CAPM Model as mentioned above to derive at the beta of the stock.

This value represents Alpha or the additional return expected from the stock when the market return is zero. A stock Xs required return is equal to the risk-free rate of return. If the beta for stock A equals zero then B.

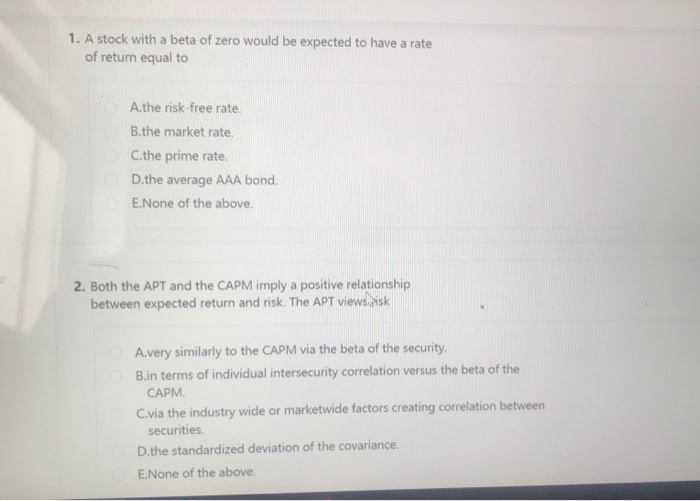

What Is Beta. Stock Xs required return is equal to the required return on the market portfol d. If the Beta for stock A equals zero then A stock As required return is equal to the risk-free rate of return.

If the Beta for Stock X equals zero then according to the CAPM a stock Xs required r. D stock As required return is greater than the required return on the market portfolio. 20 50 30 and 10.

If the beta for stock A equals zero then A. Stock A has a guaranteed return. D stock As required return is equal to the required return on the market portfolio.

If you see a beta of over 100 on a research site it is usually. Stock A gives a return of 8and stock B Gives a return of 7. It says that if your asset has a beta of zero then barr_i r_f.

If the covariance of returns between a stock and the market equals zero then what does the beta of the stock equal. Up to 256 cash back If the Beta for Stock X equals zero then according to the CAPM a stock Xs required return is equal to the risk-free rate of OneClass. B stock As required return is equal to the risk-free rate of return.

Option a Based on CAPM expected return on stock Risk free rate Beta market risk premium When beta 0 Expected return on stock Risk. If a stock moves less than the market the stocks beta is less than 10. A portfolio comprises of two stocks A and B.

The book says that The reason for this barr_i r_f is that the risk associated with an asset that is uncorrelated with the market can be diversified away. The risk-free security has a beta equal to while the market portfolios beta is equal to. Stock X has a guaranteed return.

Your portfolio earned the following returns for the years 1996 1999. A zero-beta portfolio would have the same expected return as the risk-free rate. A stock has an intrinsic value of 15 and an actual stock price of 1350.

C stock A has a guaranteed return. If the Beta for Stock X equals zero then according to the CAPM a stock Xs required return is equal to the risk-free rate of return. 14 If the beta for stock A equals zero then A stock As required return is equal to the required return on the market portfolio.

If a stock had a beta of 100 it would go to 0 on any decline in the stock market. A Zero b One c It is negative d It is positive e Need to know the variance of the market return to determine. High-beta stocks tend to be.

If a stock moves less than the market the stocks beta is less than 10. The risk-free return during the sample period is 6. β 1 exactly as volatile as the market β 1 more volatile than the market β 0 less volatile than the market.

Stock As required return is equal to the risk free ROR progressive corp. What is the Portfolio Return. A company with a higher beta has greater risk and also greater expected returns.

Such a portfolio would have zero correlation with market movements given that its expected return equals the. To calculate the Beta of a stock or portfolio divide the covariance of the excess asset returns and excess market returns by the variance of the excess market returns over the risk-free rate of. It is used as a measure of risk and is an integral part of the Capital Asset Pricing Model CAPM.

Both stock and the market or the benchmark will move in the opposite direction. If the Beta is equal to zero then this implies no relationship between the movement of the returns of. We have the following data as.

The variance of the return is then. Stock A has a weight of 60 in the portfolio. A stock that swings more than the market over time has a beta greater than 10.

Suppose we purchase an equal-weighted portfolio of n stocks. The beta coefficient can be interpreted as follows. I use the word implies because beta is based on historical data and we all.

B stock As required return is greater than the required return on the market portfolio. 0. Stock Xs required return is equal to the stocks standard deviation.

How to Calculate the Beta Coefficient. The bonds are most likely to be called if. Stock As required return is equal to the risk-free rate of return.

For example a beta of 20 or -20 would imply volatility twice the benchmark. View the full answer. Any beta below zero would imply a negative correlation with volatility expressed by how much under zero the number is.

High-beta stocks are supposed to be riskier but provide higher. Exp rate of return 7 market rate of return 8. On the other hand the investor must expect the stocks price to fall when general market fall and by a similar percentagebut a stock with a beta of 0 zero closely counter-matches the market.

Stock X has a guaranteed return. A fund with a beta of 080 is 20 less sensitive or volatile and a fund with a beta of 120 is 20 more sensitive or volatile. Alpha Measures an Asset Managers Performance.

Stock As required return is equal to the required return on the market portfolio.

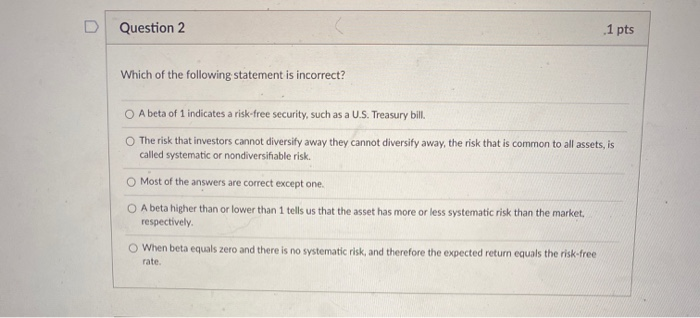

Solved Question 2 1 Pts Which Of The Following Statement Is Chegg Com

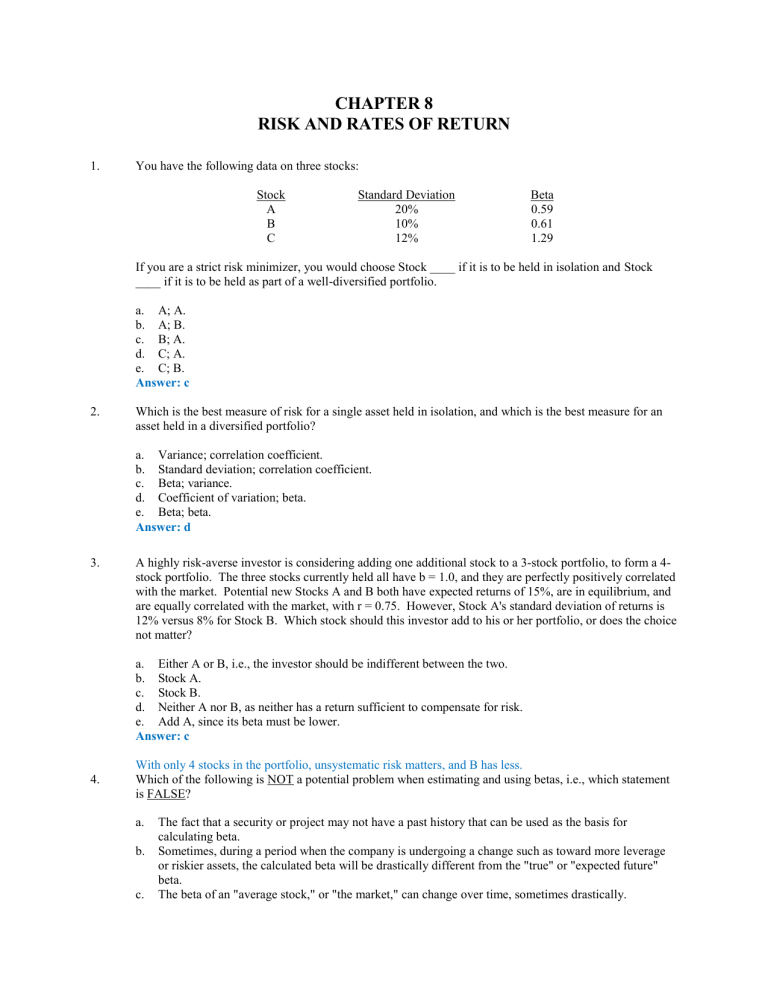

Chapter 8

Solved 1 A Stock With A Beta Of Zero Would Be Expected To Chegg Com

Comments

Post a Comment